By Daniel Pitaluga, Wealth Manager, Abacus Financial Services

One of my fondest childhood memories is listening to my grandmother repeat the same personal financial advice every time she gave me a few pounds: “don’t spend it all in one go.” Although I often chose to neglect her wise words, and instead opted to buy as much ice cream or candy as those happy pounds would allow, I now look and understand the importance of her message: saving is very important.

However, the lesson that I had to learn myself, which I often discuss with clients, is that saving alone won’t increase your standard of living significantly. This is especially true in times like today, where inflation not only reduces our ability to save – compared to last year, diesel and food now represent a significantly larger slice of everyone’s budget – but it also reduces the value of our hard-earned savings.

HM Government of Gibraltar last published its quarterly inflation data* (the index of retail prices, a broad measure that attempts to calculate the cost of living) in April 2022, showing that prices, in general, rose by 7.6% when compared to April 2021. In simple terms, saying “the inflation rate went up by 7.6%,” is the same as saying that the average Gibraltar resident’s cost of living increased by 7.6% and that every £1 they have deposited in a non-interest-bearing account, can now only buy £0.924’s worth of groceries. Inflation is a stealthy and penalising tax.

It gets even worse. By doing some simple maths, we can calculate that if inflation averages 5% over the next 10 years, the £1 you have today will only be worth £0.60 in 2032.

Fixed income

If upon retiring, you decide to downsize and invest the leftover proceeds in fixed income paying 5% interest per year, and that is your main source of income, you will be disap – pointed when you notice that the interest you receive is no longer enough to meet your monthly budget and that you’re forced to either reduce spending or tap into other savings you may have. The picture is likely to be even worse when the July figures are re – leased. For reference, May’s inflation figure in the UK came out at a surprisingly high 9.1%: In other words, £1 in May 2021 can now only buy £0.909 worth of goods and services.

Before we move away from the doom and gloom of inflation, let us look at the most recent budget update from Gibraltar’s Chief Minister, and what it means for the immediate outlook for inflation. The £45.3 million budget deficit immediately stands out, together with the expected increase in net debt of £11.5 million. Inflation has a centuries- old history of association with worsening government finances and debt increases. Furthermore, in their speeches, central bank leaders suggest that until we see a resolution in 1) the Russia-Ukraine war and 2) covid- induced supply chain disruption, inflation is likely to persist at elevated levels.

What can you do to (try) keep up with inflation?

I’ve addressed how fixed interest investments aren’t the solution to inflation-proofing your income and wealth, and for obvious reasons, leaving money in the bank earning less than 1% interest also won’t do any good when your purchasing power is being eroded by 7% and more every year. So, what can you do?

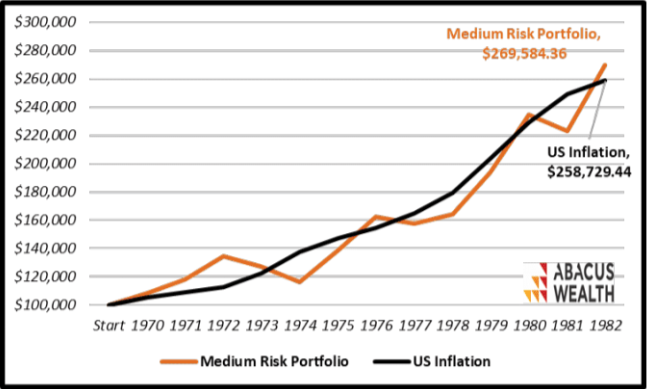

To help us answer this, let’s look at the 1970-1982 period and use data available for the USA. Throughout this period, inflation grew at an average rate of 7.64% per year, oscillating between 3.30% (1971) and 13.30% (1979). This was indeed a very challenging period for savers. In the chart below, we compared how $100,000 growing in accordance with the annual USA inflation rate performed VS an investment in a theoretical medium-risk portfolio (60% stocks, 30% fixed income, 10% commodities). In this exercise, we also included a 1.30% total annual cost ratio on the medium-risk portfolio.

Source: Abacus Wealth Management

Conclusion

During times of rising inflation, if investors don’t want to see the value of their savings eroded, it is essential that they learn not to put all their eggs in one basket. Besides being diversified, it’s equally important that they allocate a proportion of their portfolios to risky instruments like stocks, as some blue-chip companies can pass on some of their rise in costs to consumers. Thus, they provide an important inflation-protection element to portfolios.

* Source: https://www.gibraltar.gov.gi/press-releases/index-of-retail-prices-7985