by Eric Verleyen Societe Generale Private Banking Hambros (SGPBH) Chief Investment Officer

In general, 2013 was clearly a great year for equities and risky assets. The so-called “fall of safe havens” fully unfolded early in the year when US and German government bonds declined and gold dropped as economic improvements materialised. This meant that portfolios with higher tolerance for risk generally did very well in 2013 as we took advantage of the opportunities markets offered. We also were very cautious of government bonds, anticipating the poor returns from this market.

As economic improvement gradually emerged in published data, the prospect of interest rate rises no longer seemed quite so distant and longer-term interest rates rose in response.

By focusing on shorter duration bonds, high yield, subordinated bank debt and floating rate instruments we have managed to produce positive returns from fixed income in a difficult environment. Client portfolios have, therefore, done well overall and enjoyed healthy returns.

For the financial community it was a remarkable year as the Nobel Prize in Economics was attributed to Professors Eugene Fama, Lars Peter Hansen and Robert Shiller “for their empirical analysis on asset prices”. According to our records, it has been 23 years since the Nobel Academy last distinguished a work that relates to investor needs in terms of investments, asset allocation or strategy.

Looking ahead, 2014 appears that it will be a year of further economic “normalisation”, which should remain supportive for cyclical and risky assets, especially in advanced economies. The call for better economic prospects in 2014 remains unchanged, but our confidence is now higher. There is clearly better visibility, with fewer identified uncertainties. For example, geopolitical tensions have greatly eased, Eurozone sovereign stress has waned and the US fiscal dispute is over.

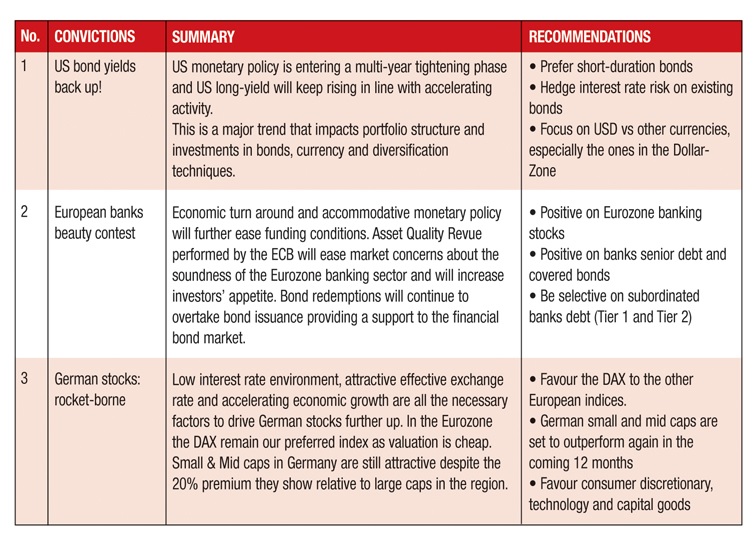

In fact, there are even more potential positive surprises ahead: Japan’s economic policies may prove a success thanks to innovative initiatives, Eurozone structural reforms on internal competitiveness could be decided and China might surprise the world by succeeding in a smooth transition from its planned export-driven economy to a liberalised consumer-driven economy, averting a hard landing. International investors increasingly share the sentiment of better visibility, currently driving asset prices higher. (Three of our seven conviction ideas for 2014– see box below).

This trend should continue. In a world of low interest rates and abundant liquidity, stocks and high-yield bonds still have room to appreciate further. Whilst interest rate rises are nearer, we do not expect them this year in Europe, UK or the US. We expect some “tapering” (reduction in bond buying) by the Federal Reserve (FED) shortly, but liquidity will remain very good and after a short period of adjustment we expect markets to remain supported by growth and strong corporate earnings.

Yet, we cannot help tempering our optimism for 2014 with some reminders of caution. Improved visibility on what is known should not to be confused with lower risks overall. The world is, of course, full of uncertainties and surprises. Keeping in mind Robert Shiller’s impressive record of tracking investor exuberance by warning for bubbles in 2000 and again in 2005-2007, we have to remember his conclusions:

l Long-term asset returns are conditioned by structural equilibrium in economic conditions, such as interest rates, growth rate and corporate profitability. This equilibrium prevails over cyclical fluctuations. Over long periods, the main economic drivers such as unemployment, profits or inflation, revert to their average trends.

l Therefore, relevant predictors of long-term returns are not short-term trends but valuation metrics that show the relationship between asset price and a long-term average of an economic indicator such as stock index/ GDP, stock prices/tangible assets, stock prices/profits, bond yield/average inflation. Note that these metrics do not give any valuable information for short-term returns.

l Bubbles do exist, and appear when investors fall prey to “irrational exuberance” confusing short-term market trends with long-term expected returns. In conclusion, beware of possible market exuberance building up in 2014 as global growth accelerates, thus be ready to reverse positions if needed. Most asset prices could perform well given current economic and financial conditions, but this is not a guarantee of extraordinary long-term returns, especially if the current conditions are themselves extraordinary. In non-Nobel wording: “tall trees can’t grow to the sky.”

www.privatebanking.societegenerale.com/hambros